Winter temperatures may be upon us, but there is still time to prepare your home before the first big freeze of the season.

Water has a unique property in that it expands in volume as it freezes. If it happens to freeze inside of a container or a pipeline, the pressure buildup of the expanded ice can cause the container or pipe to burst, resulting in damage and expensive repairs.

How to Protect Your Pipes

To protect your pipes in the winter, wrap exterior hose bibs and exposed pipes with insulation. When expecting a hard freeze, leave cabinet doors open to sinks located on exterior walls, and set your faucets to a very slight drip. Even a small amount of moving water can be sufficient to prevent water from freezing completely in the pipes.

Extended temperatures cold enough to cause pipes to freeze are uncommon in our region, but not impossible. If you are planning to be away from home for an extended period of time this winter, it may not be a good idea to turn the heater completely off while you are away - especially if the region is expecting inclement weather. Leaving the heater on at a reduced temperature, and opening cabinets to encourage warm airflow around pipes may be less expensive than turning the system off and returning home to costly plumbing repairs.

If, after a hard freeze, you turn on your sink and notice drastically reduced water pressure, you may want to suspect a frozen pipe somewhere down the line. If this occurs, your safest option is probably to contact a licensed plumber to assess the situation. If it’s feasible to do so, you may try to apply heat to the pipe gently with heated towels or a heating pad. Do not use blowtorches or any type of flammable material to attempt to thaw frozen pipes!

Now is a good time to walk around your home to identify any exposed pipes with the potential to freeze and insulate them before the harshest weather arrives. When checking your home, don't forget about your sprinkler system! Sprinkler systems that run during freezing temperatures can create hazardous conditions on roads and sidewalks. To avoid receiving a water violation for watering during rain or freezing temperatures, make sure your system is set to the "off" position when expecting inclement weather.

Attention: Click here to view a mobile-friendly version.

Best States for Retirement

Considering the following factors:

Affordability

Economic Health

Crime Rates

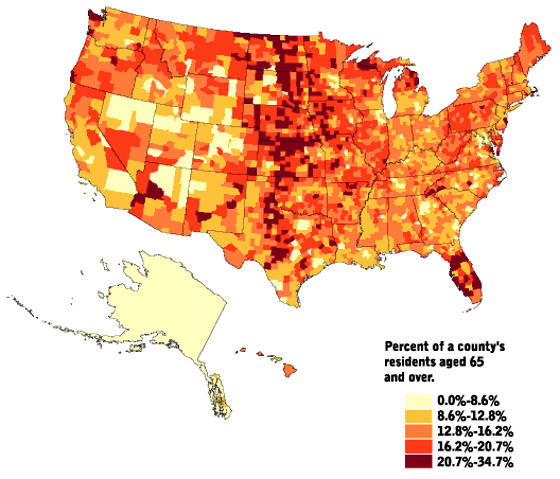

Populations of residents age 65+

Tax situation for retirees (see [3,5,8,9,12,17,18,23,30])

Kiplinger has ranked the following states as the "Best States for Retirement 2016":

South Dakota

Utah

Georgia

Tennessee

Alabama

South Carolina

Washington

Florida

Arizona

Idaho

Worst States for Retirement

Similarly, based on the following considerations:

Total population

Share of population 65+

Cost of living

Health care costs

Median home value

Average income for 65+ households

Retiree tax picture

Communities and activities

Intellectual environment

Outdoor activities

Kiplinger has ranked the following states as the "Worst States for Retirement 2016":

New York

New Jersey

California

Connecticut

Illinois

Massachusetts

Rhode Island

Montana

Vermont

Wisconsin

Indiana

Kentucky

Maine

West Virginia

Minnesota

Indiana

Final Words

The US Census Bureau recently released population estimates for the 50 states and DC. The release included data on how many people moved into and out of each state. The Northeast and Midwest tended to have more people move out than move in, while the South and West tended to have the opposite (see below diagram).[46]

Choosing the best place to retire is a personal decision. No amount of number-crunching can make it for you. Only you can decide how close to your grandkids you want to live or whether you want to hit the road or even head abroad.

The Silver State is one of nine in the U.S. that impose no income tax. Median property tax on Nevada's median home value of $165,300 is $1,423, according to the Tax Foundation.

Food and prescription drugs are exempt from the state’s 6.9% sales tax, but counties may tack on up to 1.3%. The average combined state and local sales tax rate is 7.9%.

In addition to sales taxes, vehicle owners are charged an annual “government services tax” that’s based on the vehicle’s value and age. Tax on a two-year-old vehicle with an original sticker price of $20,000 would be $238.

1. New York 2. New Jersey 3. Connecticut 4. California 5. Wisconsin 6. Minnesota 7. Maryland 8. Rhode Island 9. Vermont 10. Pennsylvania 11. Massachusetts 12. Arkansas 13. Illinois 14. Maine 15. Delaware 16. Oregon 17. North Carolina 18. Ohio 19. West Virginia 20. Hawaii 21. Michigan 22. Indianan 23. Kentucky 24. Idaho 25 Nebraska

Based on the effective tax rate for single taxpayers earning a taxable income of $50,000.

Based on a range of variables, including crime rates, employment growth, access to restaurants and attractions, educational attainment, and housing affordability, 24/7 Wall St. identified America’s 50 Best Cities to Live.

1. Harlingen, TX 2. Pueblo, CO 3. Norman, OK 4. Memphis, TN 5. Idaho Falls, ID 6. Youngstown, OH 7. Johnsboro, AK 8. Wichita Falls, TX 9. Temple, TX 10. Augusta, GA

Based on Cost of Living Index which measures prices for housing, groceries, utilities, transportation, health care, and miscellaneous goods and services

(Kyodo News) "The data showed, for example, more than 1.48 million becquerels (40 microcuries) of radioactive caesium per square meter was detected in soil at a location some 250 kilometers away from the Chernobyl plant. In the case of the Fukushima Daiichi plant, the distance was much smaller at about 33 km, the officials said."

1. Vermont 2. Connecticut 3. Rhode Island 4. Minnesota 5. Oregon 6. Montana 7. California 8. Nebraska 9. New Jersey 10 New York 11 Massachusetts 12. Utah 13. Indiana 14. Maine 15. North Dakota

1. Philadelphia, PA 2. Bridgeport, CT 3. Newark, NJ 4. Milwaukee, WI 5. Detroit, MI 6. Providence, RI 7. Baltimore, MD 8. Los Angels, CA 9. Portland, ME 10. Columbus, OH

1. Seattle, WA 2. Oakland, CA 3. Chicago, IL 4. Memphis, TN 5. Nashville, TN 6.Los Angeles, CA 7. Long Beach, CA 8. New Orleans, LA 9. New York, NY 10. San Jose, CA, San Francisco, CA (tie)

1. Hawaii 2. New York 3. Illinois 4. South Dakota 5. Wyoming 6. Indianan 7. Wisconsin 8. Pennsylvania 9. Minnesota 10. Ohio 11. New Jersey 12. Iowa 13. Vermont 14. Delaware 15. Connecticut 16. Nebraska 17. West Virginia 18. Louisiana

1. Austin, TX 2. San Francisco, CA 3. Dallas, TX 4. Seattle, WA 5. Salt Lake City, UT 6. Ogden, UT 7. Orlando, FL 8. San Jose, CA 9. Raleigh, NC 10. Cape Coral, FL 11. Denver, CO 12. San Diego, CA 13. Oakland, CA 14. Charlotte, NC 15. Phoenix, AZ 16. Portland, OR 17. Boise City, ID 18. Las Vegas, NV 19. North Port, FL 20. Fort Lauderdale, FL

1. Abilene, TX 2. Auburn, AL, 3. Austin, TX 4. Bellingham, WA 5. Blacksburg, VA 6. Bluffton, SC 7. Boise, ID 8. Bowling Green, KY 9. Brevard, NC 10. Cape Coral 11. Charleston, SC 12. Clemson, SC 13. Fargo, ND 14. Frederisksburg, TX 15. Las Cruces, NM 16. Morgan Town, WV 17. Ogden, UT 18. Oklahoma City, OK 19. Pittsburgh, PA 20. Port Saint Lucie, FL 21. Salt Lake City, UT 22. San Angelo, TX 23. State College, PA 24. Tuscon, AZ 25. Venice, FL

1. California 2. Vermont 3. Alaska 4. Maine 5. West Virginia 6. Georgia 7. New York 8. Florida 9. Texas 10. Illinois 11. Mississippi 12. Michigan 13. Arizona

1. Abilene, TX 2. Apache Junction, AZ 3. Athens, GA 4. Bella Vista, AK 5. Blacksburg, VA 6. Bluffton, SC 7. Brevard, NC 8. Cape Coral, FL 9. Clermont, FL 10. Colorado Springs, CO 11. Columbia, MO 12. Corvallis, OR 13. Fargo, ND 14. Grand Prairie, TX 15. Largo, FL 16. Lexington, KY 17. Lincoln, NE Meridian, ID 19. Mount Airy, NC 20. Pittsburgh, PA 21. San Marcos, TX 22. Smyrna, TN 23. Traverse City, MI 24. The Villages, FL 25. Walla Walla, WA

1 California 2 New York 3 Texas 4 Pennsylvania 5 Florida 6 Ohio 7 Illinois 8 Massachusetts 9 Michigan 10 New Jersey 11 North Carolina 12 Minnesota 13 Washington 14 Arizona 15 Indiana

BREAKING: Medicare Part D Premium Costs Confirmed For 2025 (YouTube link)

Who is eligible for Medicare?

U.S. citizens or legal residents with at least five consecutive years

Individuals age 65 or older

Individuals younger than 65 with a qualifying disability

Anyone with a diagnosis of end-stage renal disease or ALS

Health Care Costs

Qualifying for Medicare doesn't mean that all your health care costs will be covered. Take a note of the following marketing shenanigan:

Potential costs per month or year

According to AARP, basic coverage still costs seniors, on average, more than $3,000 a year, thanks to premiums and deductibles. And if you sign up for a Medicare supplement to help cover additional out-of-pocket expenses, that could cost you another several hundred dollars a month.

Potential lump-sum costs

Fidelity estimates that a couple who retires in 2013 will need as much as $240,000 beyond their Medicare coverage to pay for health care costs in retirement.[1]

The estimate covers deductibles and copayments, out-of-pocket expenses for prescriptions and visits to specialists, as well as other expenses, like dental visits, hearing aids, and eyeglasses — all of which aren't covered under Medicare.

The only lesson here is that you need to have adequate savings set aside for your health care in retirement.

Age 65

Starting at age 65, you can enroll in Medicare.[1] You no longer have to rely on employer-sponsored or private health insurance plans. There are 2 main ways to get your Medicare coverage:

You can apply for Medicare online by visiting the Medicare section of the Social Security website. Note that you can apply Medicare online even if you are NOT ready to retire—read Publication No. 05-10043 and the below article:

You need to register for Medicare benefits during a seven-month window, including the three months before your 65th birthday, to avoid paying higher premiums for coverage.

IEP vs AEP

If you aren't receiving Social Security or RRB benefits when you turn 65, you will have to sign up for Medicare A and/or Part B during your Initial Enrollment Period (IEP). This enrollment period begins three months before your 65th birthday, includes the month that you turn 65, and ends three months later.

During the annual enrollment period (AEP) you can make changes to various aspects of your coverage. You can switch from Original Medicare to Medicare Advantage, or vice versa. For 2022 plan, open enrollment will run from October 15, 2021, to December 7, 2021.

Figure 2. 7 Possible Medicare Combinations

7 Possible Medicare Combinations

Medicare isn't one-size-fits-all. You can combine different Medicare parts and plans to get the coverage you want. For example, there are seven possible combinations (see Figure 2):

Original Medicare (Parts A and B) or just Part A or just Part B

Original Medicare (Parts A and B) plus a stand-alone Part D plan

Original Medicare (Parts A and B) plus a stand-alone Part D plan plus a Medicare supplement plan

Original Medicare (Parts A and B) plus a Medicare supplement plan

A Medicare Advantage (Part C) plan with built-in drug coverage

A Medicare Advantage (Part C) plan without drug coverage

A Medicare Advantage (Part C) plan without drug coverage plus a stand-alone Part D plan

Only works with certain Medicare Advantage plan types

Things You Can Do During the Open Enrollment Period

Join a Medicare Prescription Drug (Part D) Plan

Switch from one Part D plan to another Part D plan

Switch from a Medicare Advantage Plan to Original Medicare

Change from one Medicare Advantage Plan to a different Medicare Advantage Plan

Switch from a Medicare Advantage Plan that doesn't offer prescription drug coverage to a Medicare Advantage Plan that does offer prescription drug coverage

Medicare Part A

What Medicare Part A (hospital insurance) covers includes:[12]

Inpatient care at a hospital

Skilled nursing facility (SNF)

Hospice.

Part A also covers services like lab tests, surgery, doctor visits, and home health care.

Most people benefit by enrolling in Medicare Part A at age 65, whether or not they continue to work. There are no premiums, and enrolling now will help you avoid potential penalties or delays down the road.

If you're covered by your employer's plan and your company has 20 or more employees, that plan remain your primary coverage. If you work for a company with fewer than 20 employees, Medicare will be your primary insurer.

Medicare Part B

What Medicare Part B (medical insurance) covers includes:[12]

Doctor and other health care providers' services

Outpatient care

Durable medical equipment

Home health care

Some preventive services

Medicare Part Bhas high-income premium surcharges, you many be better off sticking with your employer plan if you still work. Once you leave your job, you have eight months to enroll in Part B, or face a penalty.

A Medicare law requires some higher income persons to pay higher premiums. The law applies to premiums for Medicare Part B (Medical Insurance), prescription drug prescription coverage, and Medicare Part B Immunosuppressive Drug coverage.

Medicare will contact the IRS to get information about your income, If they decide that you have to pay higher premiums, they will send a a letter explaining their decision. If you disagree with the decision, you have the right to appeal.

You have 60 days to ask for an appeal in writing by using "Request for Reconsideration" form, SSA-561-U2.

What's Not Covered by Part A & Part B?

Some of the items and services that Medicare doesn't cover include:[13]

There are specific times when you can sign up for these plans, or make changes to coverage you already have. You don’t need to sign up for Medicare each year. However, each year you’ll have a chance to review your coverage and change plans.

For prescription drug coverage, Medicare-eligible individuals may enroll in one of below options:

Adding a Medicare Prescription Drug Plan (Part D)

Getting a Medicare Advantage Plan (Part C) such as an HMO or PPO that offers Medicare prescription drug coverage

Staying with one of your employer prescription drug plans which offer creditable coverage.

You can join a Medicare Prescription Drug Plan when you first become eligible for Medicare and each year from October 15th to December 7th. Similar to Medicare Part B, Medicare Part D also has high-income surcharges, you may be better off sticking with your employer plan if you still work. However, you should know that if you drop or lose Creditable Coverage offered by your employer, you should join a Medicare Prescription Drug Plan as soon as possible.

Remember that: if you go 63 continuous days or longer without creditable prescription drug coverage, your monthly premium may go up by at least 1% of the Medicare base beneficiary premium per month for every month that you did not have that coverage.

For example, if you go 19 months without Creditable Coverage, your premium may consistently be at least 19% higher than the Medicare base beneficiary premium. You may have to pay this higher premium (a penalty) as long as you have Medicare Prescription Drug coverage. In addition, you may have to wait until the following October to join.

To find out which plans cover your drugs. click here. Note that when comparing your choices, look at the estimated "Yearly Drug & Premium Cost." A plan with the lowest monthly premium may not always offer you the lowest total cost.

Further Considerations

Finally, there are some details that you might also want to consider:

Medicare doesn’t cover care provided abroad.[9]

Once you enroll in Medicare, you're no longer eligible to contribute to a health savings account (HSA; note that this is not FSA or Flexible Spending

Account).[11,27]

If you're relying on your HSA to boost your savings, you'll need to postpone Medicare.

Medicare probably won't pay for long-term care

Even if it does, it will only cover you for up to 100 days

With the annual cost of a nursing facility averaging around $78,000, it's the kind of expense that can quickly wipe out your nest egg.

Medicare premiums will be going up for many[15,16]

Call your State Health Insurance Assistance Program for personalized help

Call 1-800-MEDICARE (1-800-633-4227). TTY users should call 1-877-486-2048.

Medicare Part D Prescription Drug Plan - Notice of Creditable Coverage

Medicare Prescritption Drug coverage became available in 2006 to everyone with Medicare.

if you will become Medicare eligible in the next 12 months, pay attention to this

for more information about Medicare Prescription Drug Plan coverage, visit www.medicare.gov

if you have limited income and resources, extra help paying for Medicare Prescription Drug coverage is available. For information about this extra help, visit Social Security on the web at www.socialsecurity.gov.

it is very important that you retain this Creditable Coverage notice (from your company). If you decide to join one of the Medicare Prescription Drug Plans, you may be required to provide a copy of this notice when you join to show wether you have maintained Creditable Coverage and, therefore, whether or not you are required to pay a higher premium (a penalty).

The federal agency that oversees the Medicare program.

Many Medicare beneficiaries have other insurance in addition to their Medicare benefits. Sometimes, Medicare is supposed to pay after the other insurance. However, if certain other insurance delays payment, Medicare may take a "conditional payment" so as not to inconvenience the beneficiary, and recover after the other insurance pays.

Based on estimation, our shower cartridge may have been used for at least 14 years. Now it starts dripping. Here we discuss how to remove and replace it (i.e. a Moen shower cartridge).

Before You Start

For any plumbing project, you need to turn off water at the shutoff valve and drain remaining water from the faucet first.

Depending on where you live (i.e., cool or warm area), your water shut-off valves may locate at different areas of your house.[1,2] In a small Texas town where I live now, the main water shut-off value is located inside the meter box near the curb.

In our city, only authorized city personnel are allowed to open and work in the meter box. However, most newer homes in our area have additional shut-off valves located near the house in the flower bed. After locating the valve, you shut if off by turning it clockwise and on by turning it counter-clockwise. Finally, depending on the size of your house, draining remaining water from the pipe may take about 10 minutes.

Choosing the Right Cartridge

As shown in [3], there are different types of Moen cartridge:

1220

1222

1225

Our cartridge has two white wings as shown in the picture and it's a Moen 1222 single handle cartridge (or Posi-Temp).

How to Remove and Replace?

Without repeating, you can watch video's from youtube from the reference list for instructions. Just one additional reminder, if you run into a cartridge which won't be removed easily. you should consider using a core puller as shown above with the removal process (watch [6] for instructions).

To see broad and persistent price inflation in an economy, we generally need two things. The first is a persistent rise in broad money supply, and the second is a physical constraint on our ability to produce more commodities, goods, or services cheaply.

In truth, inflation is all about the destruction of confidence in a fiat currency’s purchasing power. And there is no better way to do that than for the government to massively increase the supply of money and place it directly into the hands of its citizenry. In other words, helicopter money and Modern Monetary Theory (MMT) were deployed—and in a big way. The result was the largest increase of inflation in 40 years.

All 0f the above predications have come true, inflation was reported hitting 9.1% in June on 07/13/2022:[75]

Inflation hit a fresh 40-year record in June, with consumer prices increasing 9.1% over the last 12 months, the Labor Department said Wednesday. It's the fastest increase in prices since November 1981, and above what economists had expected.

If inflation comes, interest rates DO rise. In this article, we will discuss how to invest in a rising rate environment if inflation is expected among market participants.

What's Inflation?

When we talk about inflation/deflation, it is important to know whether we’re talking about monetary inflation (i.e., generally Austrian's view) or price inflation(i.e., generally Keynesian' view).[36] As we have seen recently, a rising money supply is not necessarily accompanied by rising prices (although there is a certain long-term rhythm to the two different measures).

Broad money supply and price inflation are rather correlated. The most precise way to phrase it is that:[74]

Rapid money supply growthis necessary but not sufficient to cause widespread price inflation.

In other words, price inflation always tends to happen when money supply grows very quickly, but a rapid growth in money supply does not always lead to substantial price inflation.

POV—Economists vs Regular People

Jason Furman, Obama's former CEA chief, noted that economists "tend to be less bothered" by inflation than regular people.[73]

At first this seems counterintuitive. After all, economists seem to be talking about inflation all the time. But on the other hand, given the impact of food and gasoline prices, and other highly salient items, on economic sentiment, it's clear that inflation weighs heavily in the minds of the general public.

The one area aspect of inflation that economists do tend to worry quite a lot about isinflation expectations. The fear is not so much that gasoline prices or car prices or meat prices will run hot for a couple years. Their fear is that the public psychology around inflation will change. That we'll see panic buying. That we'll see a price spiral, and that this will have destabilizing effects on general welfare. In this view, Volcker's triumph wasn't that he defeated inflation per se, but that he defeated an inflationary mindset. And so economists are mostly concerned with securing and consolidating that victory.

Figure 1 shows that in the long run, interest rates tend to remain above price inflation (investors need to earn a real rate of return), but it also shows that the wedge between interest rates and price inflation has narrowed on a secular basis. We would argue that this is because over time, the Fed-to-market reaction function has become both more efficient and more credible; it takes a lower interest rate premium today than in the past to hold down inflation expectations.

Inflation and Interest Rate

Interest rates DO rise as a result of price inflation.[15] Over the long term, price inflation (here we use Core CPI; Note that rise in inflation could be made up of rising oil prices which will affect both import and export prices. However, oil is volatile, and the rate of core inflation―ex. food and energy―is the true rate of inflation that the bond marketreacts to and also the one will influence the Fed policy) is by far the best indicator of interest rate trends (Figure 1).[1] A combination of factors has led to a secular lower profile for inflation now than in the 1970s and 80s. These factors include:

A better supply-demand balance in energy markets

The benefits of increasing globalization

At the macro level, globalization has made price inflation slow to emerge, as multinational companies can shift production around the world in response to cost pressure.[17]

The evolution of Fed policies, which now include more effective tools and more timely transmission to the real economy.

These factors have given central banks more room in increasing money supply without facing the price inflation consequences for years. Hence, central banks around the world have become more active in response to economic fluctuations. The consequence is a rising ratio of money supply or credit to GDP. By definition, this means a bigger and bigger financial system, which needs more and more income to survive.

Consumer Price Index

The official measure of price inflation is the Consumer Price Index. The composition of the CPI (consumer price index) is as follows:

However, the definition of CPI was changed substantially to include a different basket of goods, and there was a rapid rise in cheap processed foods that could more easily be mass-produced, at the cost of being less healthy. In addition, money supply could go up a lot without necessarily causing broad price inflation as measured by CPI. In summary, as Lyn Alden pointed out in her article:[74]

Broad money supply and price inflation are quite correlatedwhen there is a period of constrained resources, and can become decoupledwhen resources are unusually abundant for unique circumstances involving some sort of new area of resources or labor rapidly opening up.

Inflation Drivers

What drives price inflation? There are mainly two drivers:

Wage-price spirals

Wage-price spirals refer to the vicious cycle that occurs when rising wages lead producers to raise prices, which in turn, leads workers to demand higher wages, further driving prices higher.

Credit growth and monetary policy

Price inflation is always and everywhere a monetary phenomenon.

Easy credit and loose monetary policy have the potential to create significant inflationary pressure as increasing amounts of capital bid up limited resources.

Recession or Boom? Exposing Hidden Crises in the Mark (YouTube link)

Signs of Inflation[2]

Due to the lagging nature of the CPI and PCE[49,69] reports, they often don’t present the best forward-looking measure of inflation. Like the GDP, they are much better at telling us what has happened rather than what will happen.

Bond yields are very sensitive to inflationary expectations.[65] There are two places we can look for real-time market based inflation expectations are:[48]

The TrueFlation which track inflation based on the prices of goods and services that consumers actually purchase in their daily lives

Based on the data, global investors in aggregate are positioning themselves for roughly 2% inflation in 2021.

Good Inflation vs Bad Inflation

Inflation can be classified into good inflation vs bad inflation:[44]

"Good" inflation is wages rising faster than prices. When wages rise faster than consumer prices, households have more money to spend on consumption, and it's progressively easier for them to pay down debt and support additional borrowing.

In Japan, where the central bank and government have struggled for years to generate price inflation as the means to "re-start growth," wages have fallen by 9% in real terms since 1997.

"Bad" inflation is prices rising while wages stagnate. In "bad" inflation, prices keep rising as central bank money-printing devalues the currency, but wages don't rise along with prices. As a result, wages decline in real terms, i.e. purchasing power.

How to Invest in A Rising Rate Environment?

If you believe inflation is happening, cash is your worst enemy, and bonds can appear less favorable as rising interest rates may decrease the value of outstanding bonds. Instead, you would prefer items like stocks, gold, and real assets, which are historically good inflation hedges.[48]

Strategies employ real assets aim to have either an explicit or implicit return correlation to inflation. Real assets include inflation-linked bonds,[58]commodities[64] and real estate investment trusts (REITs)[70] or other inflation-fighting assets. This can potentially enhance portfolio diversification, mitigate inflation risk and provide more stable real (after-inflation) returns.

In the chart below, Citi bank also shows the 5 year correlations of weekly returns (sector relative returns vs 10 year UST total return). You may also base your investment on the appropriate sectors in a rising interest rate (or higher bond yields) environment.

In another chart below (click to enlarge), Janus' asset allocation model shows the firm's sector preferences in a rising rate environment.[53]

Fiscal stimulus, in Janus' view, would have a more direct impact on the real economy. The firm feels the end result would be an increase in demand-pull inflation. This demand-pull driver combined with the cost-push inflation driven by tighter labor supply and the recent reset of commodities prices to a higher range creates an environment where inflation happens.

In Janus' view, this demand-pull inflation should benefit consumer discretionary names as workers are incentivized to spend. Materials and energy firms should also effectively manage cost-push inflation, especially following the recent uptick in commodity prices.

Recession vs Inflation

Video 1. Will The Coming Recession STOP Inflation? (YouTube link)

Video 2. I-Bonds For Inflation Protection (YouTube link)

The reason why the interest rates are so low? May be that America and the world at large is growing older, retiring, and are choosing to keep their money in government bonds, and other "safe" investments, and more in cash than ever before

If so, low interest rates may not move higher as inflation goes higher as they normally have. They may continue to respond instead to a slowing and unpredictable economy.

War is always inflationary for commodity prices and would only serve to

heat up the economy faster than the new 30-year inflationary cycle would

do on its own.

Such segments include both small caps and certain defensive income

plays, like utilities — both of which have historically proved more

vulnerable to contracting valuations as real rates rise.

Statistically, the rate of increase in current government expenditures at 1.2% per year (i.e., spending growth) from 2010-2014 is historically in the deflationary zone.

Rising rate will cause pain for holders of long-duration bonds. However, in this environment dividend growers – companies with sustainable free cash flow and the ability to raise payouts over time without harming their balance sheets – look attractive.

Due to the floating-rate characteristics discussed int this article, leveraged loans tend to perform well in environments of rising rates (or expected rising rates).

In past inflationary cycles, oils had led cereals by 6 months.

It's understandable why most equity investors domestically focus on cereals when it comes to soft commodity inflation.

The majority of investment options are driven by the top three crops: corn, soybean, wheat, and arguably one could simplify it down to just following the price of corn as a tell.